Tempur Sealy trades at $55.81 per share and has stayed right on track with the overall market, gaining 12.1% over the last six months. At the same time, the S&P 500 has returned 14.2%.

Is there a buying opportunity in Tempur Sealy, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.We don't have much confidence in Tempur Sealy. Here are three reasons why you should be careful with TPX and a stock we'd rather own.

Why Is Tempur Sealy Not Exciting?

Established through the merger of Tempur-Pedic and Sealy in 2012, Tempur Sealy (NYSE:TPX) is a bedding manufacturer known for its innovative memory foam mattresses and sleep products

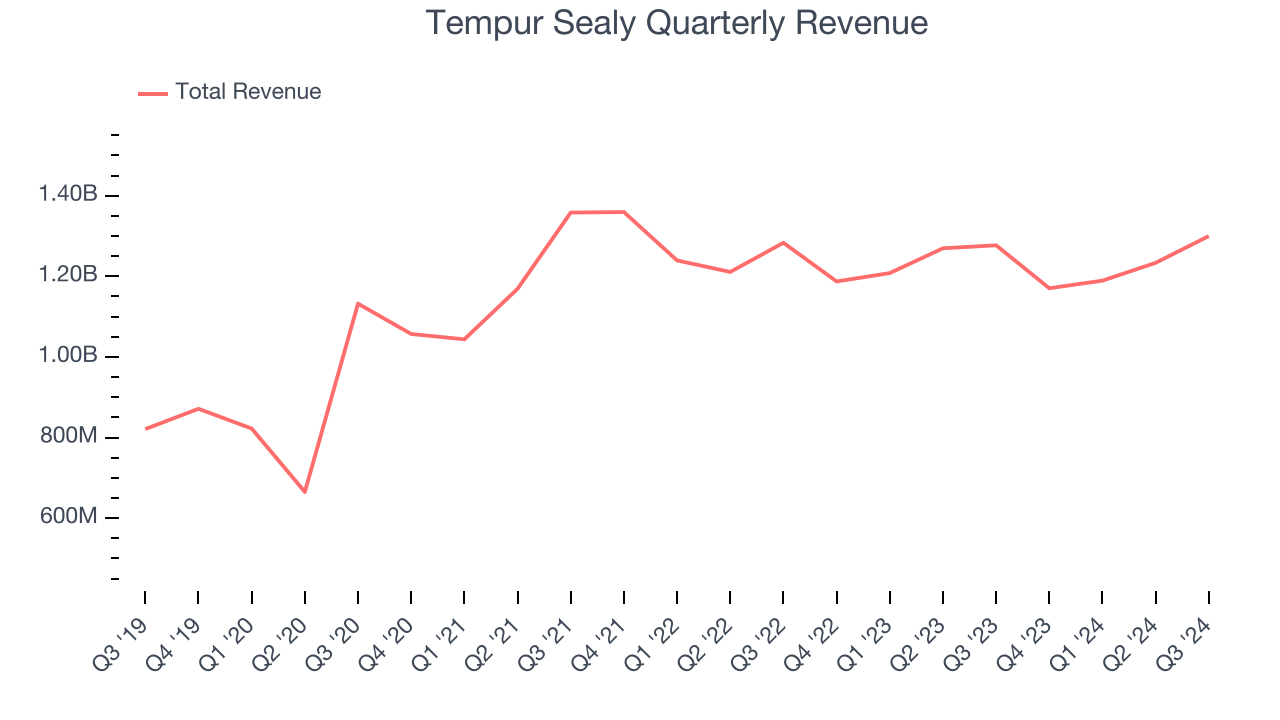

1. Long-Term Revenue Growth Disappoints

A company’s long-term sales performance signals its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Tempur Sealy grew its sales at a 10.9% compounded annual growth rate. Although this growth is solid on an absolute basis, it fell short of our benchmark for the consumer discretionary sector.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Tempur Sealy’s revenue to rise by 3.6%. Although this projection indicates its newer products and services will catalyze better top-line performance, it is still below average for the sector.

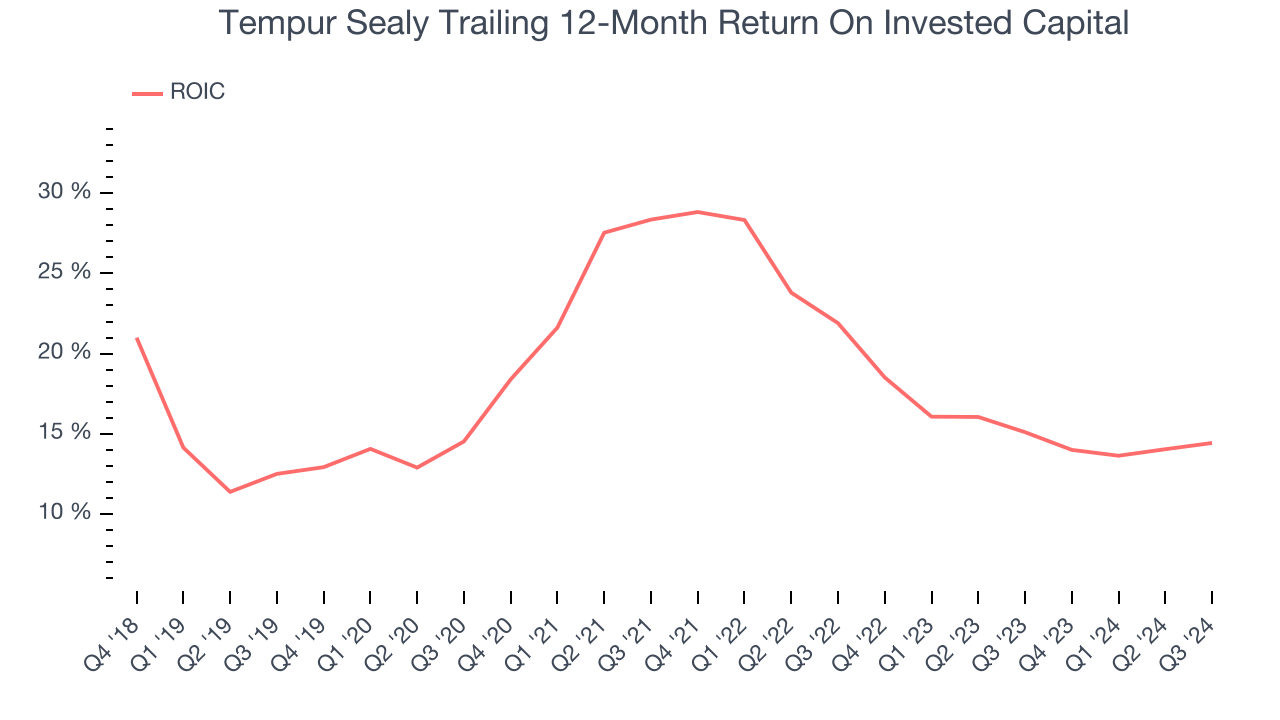

3. New Investments Fail to Bear Fruit as ROIC Declines

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We typically prefer to invest in companies with high returns because it means they have viable business models, but the trend in a company’s ROIC is often what surprises the market and moves the stock price. Over the last few years, Tempur Sealy’s ROIC has decreased. We like what management has done in the past but are concerned its ROIC is declining, perhaps a symptom of fewer profitable growth opportunities.

Final Judgment

Tempur Sealy isn’t a terrible business, but it doesn’t pass our quality test. That said, the stock currently trades at 19.9x forward price-to-earnings (or $55.81 per share). Beauty is in the eye of the beholder, but our analysis shows the upside isn’t great compared to the potential downside. We're fairly confident there are better stocks to buy right now. We’d recommend looking at Chipotle, which surprisingly still has a long runway for growth.

Stocks We Would Buy Instead of Tempur Sealy

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.