Bandwidth has followed the market’s trajectory closely, rising in tandem with the S&P 500 over the past six months. The stock has climbed by 5.9% to $17.89 per share while the index has gained 7%.

Is there a buying opportunity in Bandwidth, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.We're sitting this one out for now. Here are three reasons why BAND doesn't excite us and a stock we'd rather own.

Why Do We Think Bandwidth Will Underperform?

Started in 1999 by David Morken who was later joined by Henry Kaestner as co-founder in 2001, Bandwidth (NASDAQ:BAND) provides thousands of customers with a software platform that uses its own global network to provide phone numbers, voice, and text connectivity.

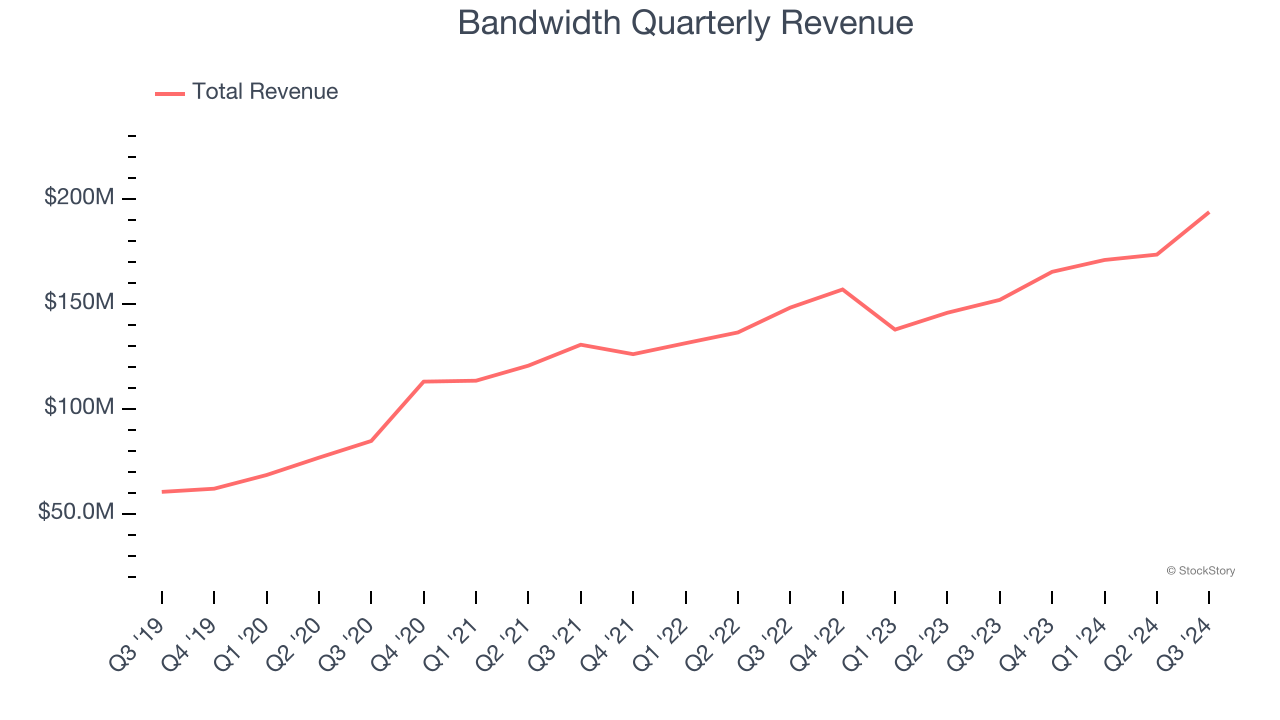

1. Long-Term Revenue Growth Disappoints

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last three years, Bandwidth grew its sales at a 13.8% annual rate. Although this growth is solid on an absolute basis, it fell short of our benchmark for the software sector.

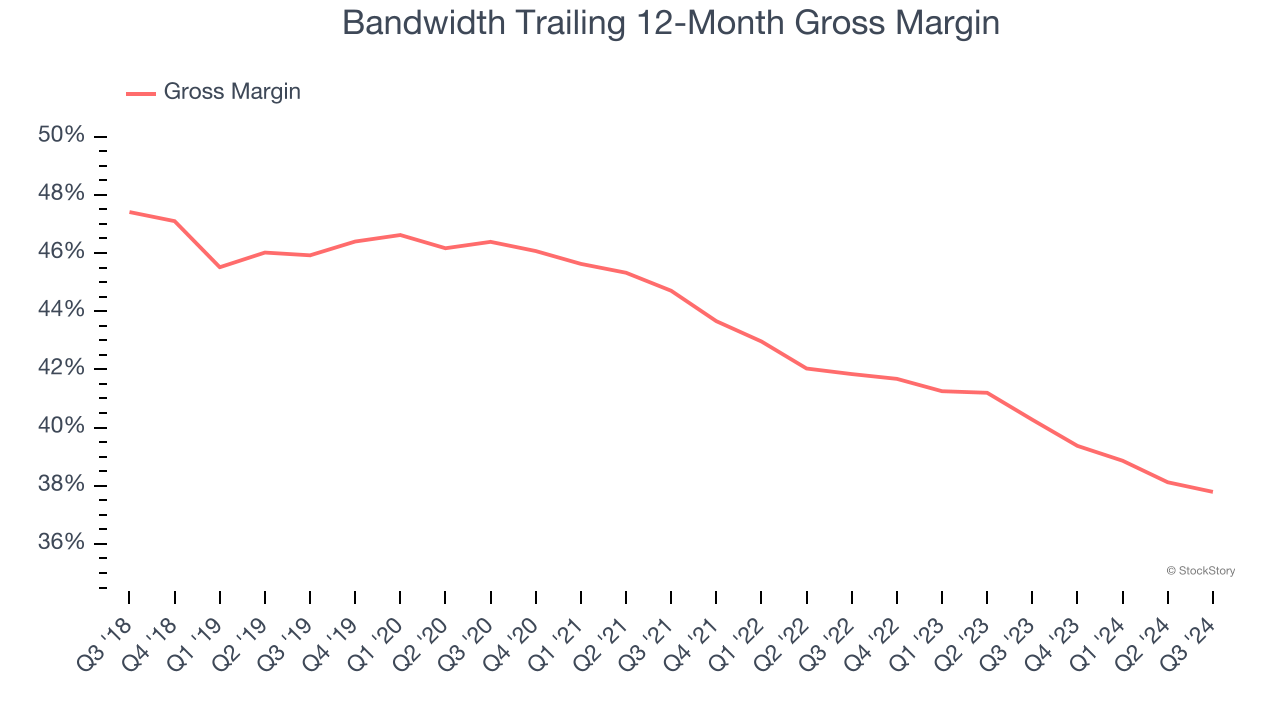

2. Low Gross Margin Reveals Weak Structural Profitability

For software companies like Bandwidth, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Bandwidth’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 37.8% gross margin over the last year. Said differently, Bandwidth had to pay a chunky $62.21 to its service providers for every $100 in revenue.

3. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Bandwidth’s revenue to rise by 6.3%, a deceleration versus its 13.8% annualized growth for the past three years. This projection doesn't excite us and indicates its products and services will see some demand headwinds.

Final Judgment

Bandwidth falls short of our quality standards. That said, the stock currently trades at 0.7× forward price-to-sales (or $17.89 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better stocks to buy right now. We’d suggest looking at CrowdStrike, the most entrenched endpoint security platform.

Stocks We Would Buy Instead of Bandwidth

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like United Rentals (+550% five-year return). Find your next big winner with StockStory today for free.